Archived information

Archived information is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Annex 4 - Debt Management Strategy for 2015–16

Highlights

- The debt program for 2015–16 is consistent with the Government’s medium‑term debt strategy and maintains the focus on stability and the reduction of financial risk.

- Gross bond issuance is expected to be $90 billion in 2015–16 and stabilize around $98 billion over the medium term. At the end of 2015–16, the stock of marketable bonds is projected to be about $507 billion.

- The Government will cease issuing 3-year bonds starting in 2015–16. This will allow for the building of larger benchmark sizes in the core 2- and 5-year sectors, which will increase liquidity and support the well-functioning of these important sectors.

- The stock of treasury bills is projected to decrease from $136 billion at the start of this fiscal year to $129 billion by the end of 2015–16.

- In 2014, the Government issued 50-year bonds for the first time. With a total of $3.5 billion issued through syndication, these bonds were well received by investors and contributed to a reduction in refinancing risk at a low cost. Given the strong demand for long-term bonds and with long-term yields remaining well below their historical average, additional 50-year bonds may be issued in 2015–16, subject to favourable market conditions.

Introduction

The Debt Management Strategy sets out the Government of Canada’s objectives, strategy and plans for the management of its domestic and foreign debt, other financial liabilities and related assets. Borrowing activities support the ongoing refinancing of government debt coming to maturity, the execution of the budget plan and the financial operations of the Government. This includes investing in financial assets needed to establish a prudent liquidity position and borrowing on behalf of certain Crown corporations.

The Financial Administration Act requires that the Government table in Parliament, prior to the start of the fiscal year, a report on the anticipated borrowing to be undertaken in the year ahead, including the purposes for which the money will be borrowed. As such, the Minister of Finance tabled the Debt Management Strategy for 2015–16 in Parliament on March 30, 2015.

The Debt Management Strategy for 2015–16 is being updated in the context of Economic Action Plan 2015 to reflect the latest fiscal and financial projections. The March 30, 2015 version of the Debt Management Strategy for 2015–16 was based on the previous fiscal and financial projections associated with the Update of Economic and Fiscal Projections released on November 12, 2014. The infrastructure package announced in November 2014 was also included in the baseline.

Planned Borrowing Activities for 2015–16

Borrowing Authority

Theaggregate borrowing limit approved by the Governor in Council to meet projected financial requirements in 2015–16 and provide a margin for prudence is $270 billion, which is unchanged from 2014–15 and $30 billion lower than in 2013–14.

Actual borrowings and uses of funds compared with those forecast will be reported in the 2015–16 Debt Management Report, and detailed information on outcomes will be provided in the 2016 Public Accounts of Canada. Both documents will be tabled in Parliament in the fall of 2016.

Sources of Borrowings

The aggregate principal amount of money to be borrowed by the Government from financial markets in 2015–16 is projected to be $231 billion.

Uses of Borrowings

Refinancing Needs

Refinancing needs, projected to be $212 billion during the year, are mainly comprised of $136 billion for maturing treasury bills and $70 billion for maturing bonds.

Financial Source/Requirement

The other main determinant of borrowing needs is the Government’s financial source/requirement. If the Government has a financial source, it can use the source for some of its refinancing needs. If it has a financial requirement, then it must meet that requirement along with its refinancing needs.

The financial source/requirement measures the difference between cash coming into the Government and cash going out. This measure is affected not only by the budgetary balance but also by the Government’s non-budgetary transactions.

Non-budgetary transactions include changes in federal employee pension accounts; changes in non-financial assets; investing activities through loans, investments and advances (including loans to three Crown corporations—the Business Development Bank of Canada, Farm Credit Canada and Canada Mortgage and Housing Corporation); and other transactions (e.g., changes in other financial assets and liabilities, and foreign exchange activities).

For 2015–16, a financial requirement of approximately $14 billion is projected. As the amount the Government plans to borrow is higher than borrowing requirements, the year-end cash position is projected to increase by about $5 billion (Table A4.1) to accommodate collateral management in support of cross-currency swap activities that fund assets in the Exchange Fund Account (EFA).

Actual borrowings for the year may differ from the forecast due to uncertainty associated with economic and fiscal projections, the timing of cash transactions and other factors, such as changes in foreign reserve needs and Crown borrowings. Therefore, the aggregate borrowing limit of $270 billion for 2015–16 includes a margin for prudence, enabling debt management operations to respond to changing circumstances without the need for frequent resubmissions to the Governor in Council.

| billions of dollars | |

|---|---|

| Sources of Borrowings | |

| Payable in Canadian currency | |

| Treasury bills1 | 129 |

| Bonds | 90 |

| Retail debt | 2 |

| Total payable in Canadian currency | 221 |

| Payable in foreign currencies | 10 |

| Total cash raised through borrowing activities | 231 |

| Uses of Borrowings | |

| Refinancing needs | |

| Payable in Canadian currency | |

| Treasury bills | 136 |

| Bonds | 70 |

| Of which: | |

| Regular bond buybacks | 0.4 |

| Cash management bond buybacks | 23 |

| Retail debt | 2 |

| Total payable in Canadian currency | 208 |

| Payable in foreign currencies | 4 |

| Total refinancing needs | 212 |

| Financial source/requirement | |

| Budgetary balance | -1 |

| Non-budgetary transactions | |

| Pension and other accounts | 0 |

| Non-financial assets | 2 |

| Loans, investments and advances | 8 |

| Of which: | |

| Enterprise Crown corporations | 5 |

| Other | 3 |

| Other transactions2 | 6 |

| Total non-budgetary transactions | 16 |

| Total financial source/requirement | 14 |

| Total uses of borrowings | 226 |

| Other unmatured debt transaction3 | 0 |

| Net Increase or Decrease (-) in Cash | 5 |

Debt Management Strategy for 2015–16

Objectives

The fundamental objective of debt management is to raise stable and low‑cost funding to meet the financial needs of the Government of Canada. An associated objective is to maintain a well-functioning market in Government of Canada securities, which helps to keep debt costs low and stable.

Raising Stable Low-Cost Funding

Achieving stable low-cost funding involves striking a balance between the cost and the risk associated with the debt structure.

Over the medium term, debt management decisions will be taken with a view to keeping debt costs low and maintaining risks at prudent levels, while reserving sufficient flexibility to adapt to changing circumstances.

Maintaining a Well-Functioning Government Securities Market

Having access to a well-functioning government securities market ensures that funding can be raised efficiently to meet the Government’s needs regardless of economic conditions. To support a liquid and well-functioning Government of Canada securities market, the Government strives to maintain transparent, regular and diversified borrowing programs.

Continued Strong Demand for Government of Canada Debt Securities

Among global investors, Canada has a well-earned reputation for responsible fiscal, economic and financial sector management. The major credit rating agencies have again accorded Canada the highest possible credit rating with a stable outlook, a position shared by very few countries. This position of strength has supported healthy ongoing demand for Government of Canada securities, making them among the world’s most sought-after investments.

- Canada

- Australia

- Denmark

- Germany

- Luxembourg

- Norway

- Singapore

- Sweden

- Switzerland

Market Consultations

As in previous years, market participants were consulted periodically in 2014–15 as part of the process of developing the debt management strategy. The most recent set of consultations were held in November 2014 and were focused on obtaining feedback on a broad range of topics associated with the functioning of the Government of Canada treasury bill and bond markets as well as the terms of participation governing Government of Canada securities auctions.

Further details on the subjects of discussion and the views expressed during the consultations can be found on the Bank of Canada website.

Medium-Term Debt Strategy

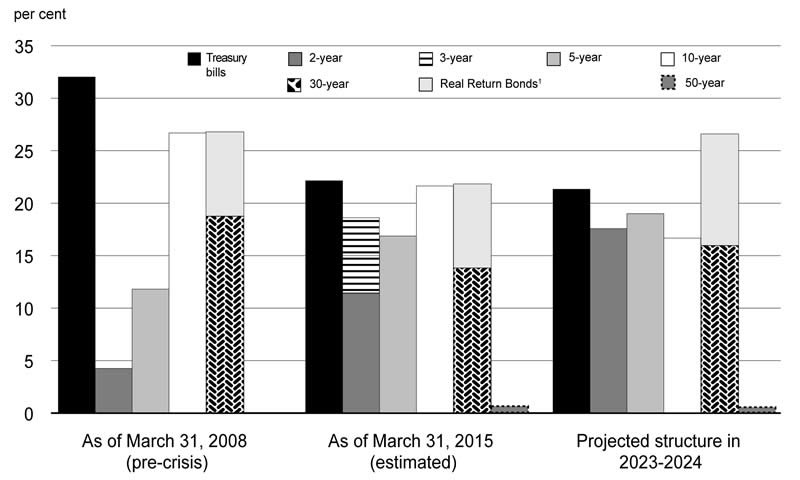

The Government’s medium-term debt strategy serves as the fundamental building block for the annual debt management strategy and is informed by modelling analysis that reflects a wide range of economic and interest rate scenarios drawn from historical experience. The medium-term debt strategy is aimed at gradually transitioning the debt structure towards a more even distribution across maturity sectors (Chart A4.1), while improving cost-risk characteristics over time. Specifically, it seeks to strike a balance between keeping funding costs low and mitigating risks to the Government, as measured by metrics such as debt rollover, the variation in annual debt-service charges and the variation in the annual budgetary balance.

1 Includes Consumer Price Index adjustment.

Source: Department of Finance.

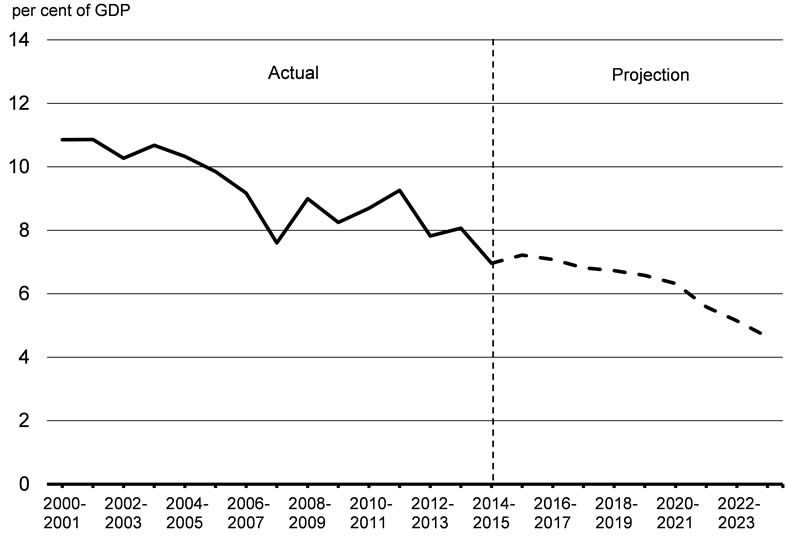

Over the medium term the share of bonds with original terms of 10 years or more is projected to remain around 43 per cent. The level of refinancing risk of domestic market debt is projected to decline over the medium term. The net annual refixing amount of domestic market debt as a percentage of gross domestic product (GDP), which measures the amount of all domestic market debt that matures within one year relative to Canada’s GDP, is projected to decline from about 7 per cent in 2015–16 to approximately 5 per cent over the medium term (Chart A4.2).

Source: Department of Finance.

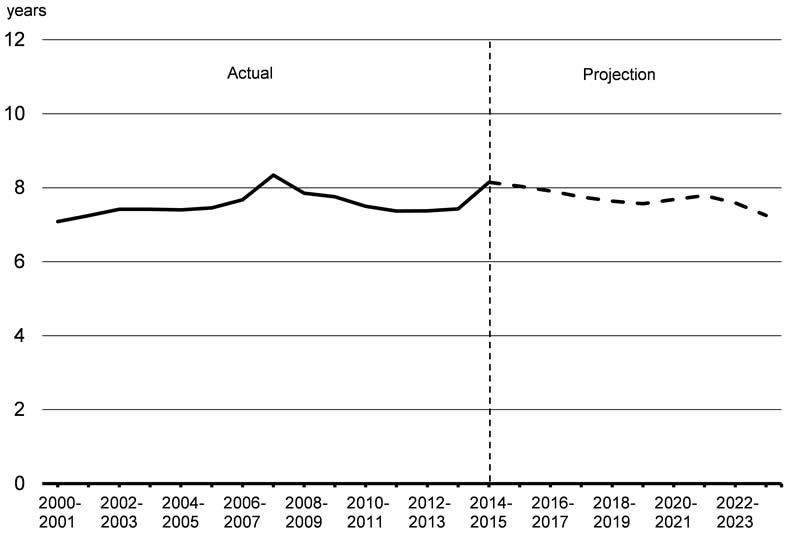

The average term to maturity of domestic market debt, net of financial assets, is projected to remain relatively stable around 7.5 to 8 years over the medium term (Chart A4.3).

Is Expected to Remain Stable

Source: Department of Finance.

Composition of Market Debt

Total market debt is projected to be $668 billion by the end of 2015–16 (Table A4.2), reflecting higher year-end cash balances, significant cash outlays on federal infrastructure, borrowings of Crown corporations, and the requirements associated with increasing international reserves.

| 2011–12 Actual |

2012–13 Actual |

2013–14 Actual |

2014–15 Estimated |

2015–16 Projected |

|

|---|---|---|---|---|---|

| Marketable bonds | 448 | 469 | 473 | 487 | 507 |

| Treasury bills | 163 | 181 | 153 | 136 | 129 |

| Foreign debt | 11 | 11 | 16 | 20 | 27 |

| Retail debt | 9 | 7 | 6 | 6 | 6 |

| Total market debt | 631 | 668 | 649 | 649 | 668 |

Debt management strategy decisions taken over the past few years have been aimed at gradually transitioning the debt structure towards a more even distribution across maturity sectors, consistent with the medium-term debt strategy.

The projected decline in the stock of treasury bills, from about $136 billion at the start of the fiscal year to approximately $129 billion by the end of 2015–16, continues to be an effective means to improve refinancing and rollover risks.

Bond Program

In 2015–16, gross bond issuance is expected to be $90 billion, representing a decrease of about $9 billion from 2014–15 levels (Table A4.3).

| 2011–12 Actual |

2012–13 Actual |

2013–14 Actual |

2014–15 Estimated |

2015–16 Projected |

|

|---|---|---|---|---|---|

| Gross bond issuance | 100 | 96 | 88 | 99 | 90 |

| Buybacks | -5.9 | -1.5 | -1.0 | -0.5 | -0.4 |

| Net issuance | 94 | 94 | 87 | 98 | 90 |

| Maturing bonds and adjustments1 | -62 | -73 | -82 | -84 | -70 |

| Change in bond stock | 32 | 21 | 4 | 14 | 20 |

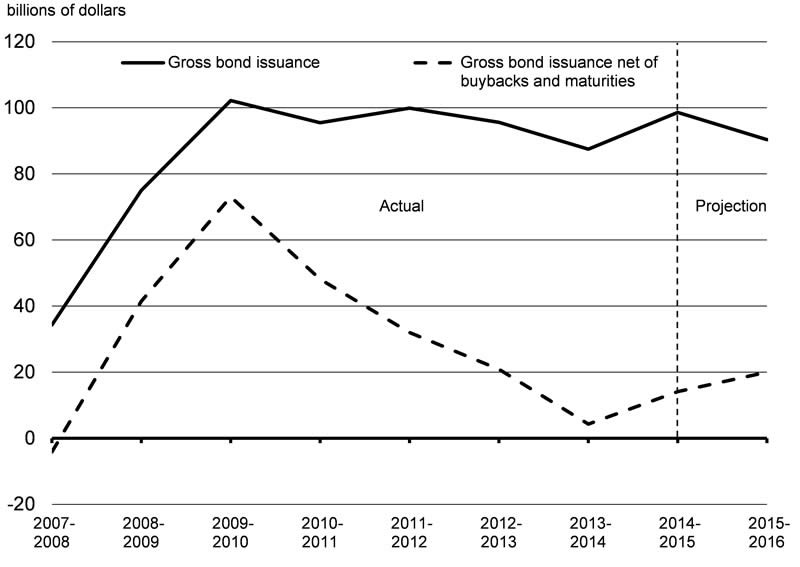

Gross bond issuance net of buybacks and maturities, or the net new supply of bonds, will increase in 2015–16 (Chart A4.4). Over the medium term, annual gross bond issuance is projected to stabilize around $98 billion.

Issuance in the 3-year sector was reintroduced in 2009 in light of significantly higher financial requirements associated with the Extraordinary Financing Framework and the stimulus phase of Canada’s Economic Action Plan.

While auctions for 3-year bonds perform well, the 3-year sector is not a core component of the Government’s debt mix (i.e., 2-, 5-, 10- and 30-year nominal bonds). In this regard, market participants have expressed a preference for the cessation of issuance in the 3-year sector in favour of increased issuance in other sectors, specifically 2- and 5-year bonds.

Consistent with the feedback received, there will be no issuance in the 3-year sector in 2015–16. The forgone issuance will be gradually reallocated to the 2- and 5-year sectors. Ceasing issuance in the 3-year sector will allow for the building of larger benchmark sizes in the core 2- and 5-year sectors, which will increase liquidity and support the well-functioning of these important sectors.

Given the strong demand for long-term bonds and with long-term yields remaining well below their historical average, additional 50-year bonds may be issued in 2015–16. Any decision to reopen the ultra-long bond would be subject to favourable market conditions and would be communicated by the Government to market participants during the course of the fiscal year.

Maturity Dates and Benchmark Bond Target Range Sizes

The bond issuance pattern for 2014–15 had a total of eight maturity dates, with the 2- and 3-year sectors sharing two maturity dates: February 1 and August 1 (Table A4.4).

| Feb. | Mar. | May | June | Aug. | Sept. | Nov. | Dec. | |

|---|---|---|---|---|---|---|---|---|

| 2-year | 8-12 | 8-12 | 8-12 | 8-12 | ||||

| 3-year | 8-12 | 8-12 | ||||||

| 5-year | 10-13 | 10-13 | ||||||

| 10-year | 10-14 | |||||||

| 30-year | 12-15 | |||||||

| Real Return Bond1 | 10-16 | |||||||

| Total | 16-24 | 10-13 | 8-12 | 10-14 | 16-24 | 10-13 | 8-12 | 10-16 |

Ceasing issuance in the 3-year sector will not change the number and pattern of maturity dates but will allow for the building of larger bond benchmarks in the 2- and 5-year sectors. The benchmark bond target range size will be $10 billion to $14 billion for the 2-, 5- and 10-year sectors, and it will be $10 billion to $16 billion for the 30-year and Real Return Bond sectors (Table A4.5). Due to the fungibility with outstanding 3-year bonds, issuance in the fungible 2-year August 1, 2017 and February 1, 2018 bonds may be smaller than the non-fungible 2-year November 1, 2017 and May 1, 2018 bonds.

| Feb. | Mar. | May | June | Aug. | Sept. | Nov. | Dec. | |

|---|---|---|---|---|---|---|---|---|

| 2-year | 10-14 | 10-14 | 10-14 | 10-14 | ||||

| 5-year | 10-14 | 10-14 | ||||||

| 10-year | 10-14 | |||||||

| 30-year | 10-16 | |||||||

| Real Return Bond1 | 10-16 | |||||||

| Total | 10-14 | 10-14 | 10-14 | 10-14 | 10-14 | 10-14 | 10-14 | 10-16 |

Bond Auction Schedule

In 2015–16, there will be quarterly auctions of 2-, 5- and 10-year bonds and Real Return Bonds. To accommodate the cessation of 3-year bond auctions in 2015–16, the number of auctions for 2- and 5-year bonds will increase. For instance, there will be four auctions for non-fungible 2-year bonds and two auctions per quarter for 5-year bonds. Each quarter will feature one 10-year auction in 2015–16. Two 30-year nominal bond auctions will occur—one in each of the first and third quarters of 2015–16.

The order of bond auctions within each quarter may be adjusted to support the borrowing program, and there may be multiple auctions of the same bonds in some quarters. The dates of each auction will continue to be announced through the Quarterly Bond Schedule that is published on the Bank of Canada website prior to the start of each quarter.

Bond Buyback Programs

Two types of bond buyback operations will be conducted in 2015–16: regular bond buybacks on a switch basis and cash management bond buybacks.

Buyback operations on a switch basis will be continued in the 30-year sector and will be conducted in the second quarter of 2015–16. No regular buyback operations on a cash basis are planned for 2015–16.1

Weekly cash management bond buyback operations will be continued in 2015–16. The cash management bond buyback program helps to manage government cash requirements by reducing the high levels of cash balances needed ahead of large bond maturities.

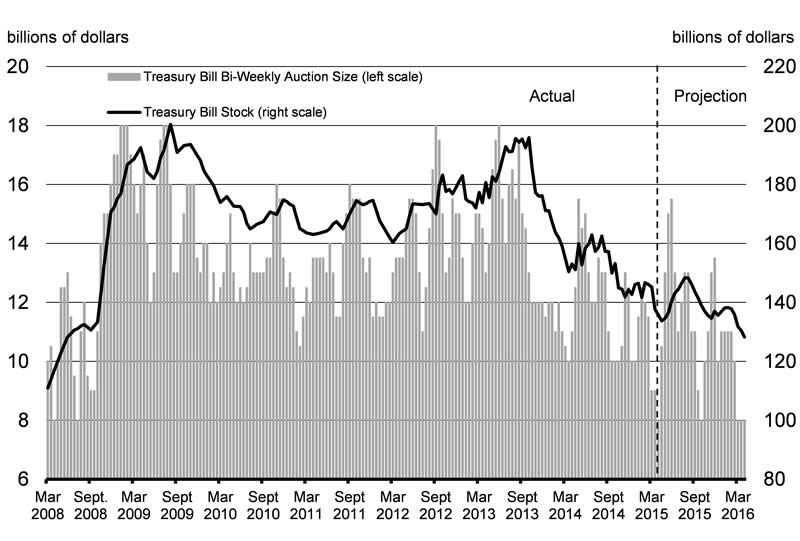

Treasury Bill Program

Over the course of 2015–16, the share of treasury bills is projected to fall from about 22 per cent to just over 20 per cent of domestic market debt. This decline is consistent with the medium-term debt strategy, which has a treasury bill target share of around 20 per cent, and maintains issuance stability in the bond program.

In accordance with this plan, the stock of treasury bills is projected to decrease from $136 billion at start of this fiscal year to $129 billion by the end of 2015–16.

Bi-weekly issuance of 3-, 6- and 12-month maturities will be continued in 2015–16, with bi-weekly auction sizes projected to be largely in the $8 billion to $12 billion range (Chart A4.5). Cash management bills (i.e., short-dated treasury bills) help manage government cash requirements in an efficient manner. These instruments will also continue to be used in 2015–16.

Source: Bank of Canada.

Prudential Liquidity and Cash Management

Prudential Liquidity

The Government holds liquid financial assets in the form of domestic cash deposits and foreign exchange reserves to safeguard its ability to meet payment obligations in situations where normal access to funding markets may be disrupted or delayed. This also supports investor confidence in Canadian government debt.

The Government’s overall liquidity levels cover at least one month of net projected cash flows, including coupon payments and debt refinancing needs.

Cash Management

The Bank of Canada, as fiscal agent for the Government, manages the Receiver General Consolidated Revenue Fund, from which the balances required for the Government’s day-to-day operations are drawn. The core objective of cash management is to ensure that the Government has sufficient cash available at all times to meet its operating requirements.

Cash consists of moneys on deposit with the Bank of Canada, chartered banks and other financial institutions. Cash with the Bank of Canada includes operational balances and balances held for the prudential liquidity plan. Cash balances are projected to increase to $33 billion at March 31, 2016 to accommodate additional cash balances needed for collateral management in support of cross-currency swap activities that fund assets in the Exchange Fund Account (Table A4.6). Periodic updates on the liquidity position are available in The Fiscal Monitor.

| 2013–14 Actual |

2014–15 Estimated |

2015–16 Projected |

|

|---|---|---|---|

| Callable deposits with Bank of Canada | 20 | 20 | 20 |

| Balances with Bank of Canada | 2 | 1 | 2 |

| Balances with financial institutions | 4 | 6 | 4 |

| Cash collateral with financial institutions | – | – | 6 |

| Total | 26 | 28 | 33 |

Retail Debt

Around 2.5 million Canadians hold Canada Savings Bonds (CSBs) or Canada Premium Bonds (CPBs). CSBs are offered exclusively through the Payroll Savings Program while CPBs are available for sale through financial institutions and dealers. Investors repeatedly cite the safety and security of CSBs and CPBs as key attributes, with payroll deduction providing a convenient, simple and free automatic savings option.

Further information on the retail debt program is available on the Canada Savings Bonds website.

Foreign Currency Funding

The purpose of the EFA is to aid in the control and protection of the external value of the Canadian dollar. Assets held in the EFA are managed to provide foreign currency liquidity, support market confidence, and promote orderly conditions for the Canadian dollar in the foreign exchange markets, if required. Liquid foreign exchange reserves are maintained at a level at or above 3 per cent of nominal GDP, consistent with the Government’s prudential liquidity plan.

The Government plans to fund the purchase of foreign currency assets through multiple sources. These include a short-term US-dollar paper program (Canada bills), medium-term notes, international bond issues (global bonds), purchases and sales of Canadian dollars in foreign exchange markets, and cross-currency swaps involving the exchange of domestic liabilities for foreign-currency-denominated liabilities. Foreign currency funding requirements for 2015–16 are estimated to be around US$9 billion, but may vary as a result of movements in foreign interest and exchange rates.

The Debt Management Strategy for 2015–16 assumes that all foreign liabilities maturing during the year will be refinanced. The mix of funding sources used to finance the reserves in 2015–16 will depend on a number of considerations, including relative cost, market conditions and the objective of maintaining a prudent foreign-currency-denominated debt maturity structure.

Further information on foreign currency funding and the foreign reserve assets is available in the Report on the Management of Canada’s Official International Reserves and in The Fiscal Monitor.

Information on Government of Canada Domestic Debt Securities

Information regarding outstanding Government of Canada domestic marketable debt securities is available on the Bank of Canada website. The legal terms and conditions for Canada’s domestic marketable debt securities are posted on the Department of Finance website.

1 Bond buyback operations on a cash basis and on a switch basis involve the purchase of bonds with a remaining term to maturity of 12 months to 25 years. Bond buyback operations on a cash basis involve the exchange of a bond for cash. Bond buyback operations on a switch basis involve the exchange of one bond for another, on a duration-neutral basis (e.g., an off-the-run bond for the building benchmark bond).