Chapter 3 - Fairness for the Middle Class and those Working Hard to Join it

Introduction

When the economy works for the middle class and those working hard to join it, it works for everyone.

Canadians work hard and should be rewarded for that work with greater opportunities for themselves, and for their families. This sense of optimism is essential to growing our economy. Over the last several decades, however, the benefits of economic growth have not been evenly shared. Over the past 30 years, the median real wage income has barely risen, leaving many Canadians concerned for their future. In contrast, among the wealthiest 0.01 per cent of Canadians, after-tax after-transfer incomes have risen dramatically. Individuals earning more than $1.8 million per year have, on average, seen their incomes rise by nearly 156 per cent in that time (or 3.1 per cent per year on average) after inflation.

The Government of Canada is committed to an economy that works for the middle class. As the economy grows, we will ensure every Canadian pays their fair share, so that the benefits of that growth can be shared by more than just a wealthy few.

In December 2015, the Government raised taxes on the wealthiest one per cent, in order to cut taxes for the middle class, benefitting 9 million Canadians. In its first budget, the Government replaced the previous child benefit system with the Canada Child Benefit, which is simpler, more generous, and better targeted to those who need it most.

The Government also took strong steps to detect, audit and combat tax evasion and aggressive tax avoidance, both at home and around the world, by boosting funding to the Canada Revenue Agency (CRA). These measures are beginning to bear fruit, with the CRA on track to recover over $5 billion in additional federal revenues over six years.

In the Fall Economic Statement, the Government is confirming that it is moving forward on proposals to fix a tax system that encourages the wealthy to incorporate, so they can get a better tax rate.

Fixing unfairness in the tax system not only fulfills our fundamental promise to middle class Canadians, it is at the heart of our plan for long-term, sustainable economic growth. As we continue with this plan, including making smart, necessary investments in our people, our communities and our economy, we will make sure that the success we create together is shared, by reinvesting in Canada's middle class, in those working hard to join it, and in programs and services that all Canadians benefit from.

New Measures: Strengthening Support for Canadian Families and Workers

In line with its commitment to strengthen the middle class, the Government is announcing measures in this Fall Economic Statement to further support Canadian families and workers. These investments will help to ensure the real value of benefits for families with children is maintained over time, and improve income security and quality of life for low-income working Canadians.

Strengthening The Canada Child Benefit

In Budget 2016, the Government introduced one of the most important and innovative social policy measures in a generation. That budget replaced the previous child benefit system with the new Canada Child Benefit (CCB)—a simpler, more generous, better targeted benefit that is entirely tax-free. During the first benefit year, over 3.3 million families received more than $23 billion in CCB payments, and the nine out of 10 families better off under the CCB received on average almost $2,300 more in benefits, tax-free. The CCB has helped lift about 300,000 children out of poverty and, by the end of this year, child poverty will have been reduced by 40 per cent from what it was in 2013.

The CCB provides greater support to those who need it most: low- and middle-income families. It puts more money in their pockets for soccer cleats, or summer camps, or to put healthy food on the table. The CCB is particularly beneficial for families led by single parents. These families are most often led by single mothers and tend to have lower total incomes, and thus benefit more from a better-targeted CCB. About 65 per cent of families receiving the maximum CCB amounts are single parents, 90 per cent of whom are single mothers.

In the fall of 2016, the Government took further action to support Canadian families over the long term by announcing that, as of the 2020–21 benefit year, the CCB would be indexed to ensure it keeps pace with the rising cost of living.

A year later, Canada's economy is growing faster than expected, thanks in part to the positive effects the CCB has had in improving consumer confidence and consumption. With this increased flexibility, and to ensure benefits of our strong growth are shared with the middle class and those working hard to join it, the Government proposes to accelerate the indexation of the CCB's benefit amounts and phase-out thresholds by two years to July 2018.

This means better support sooner to ensure that the CCB continues to play a vital role in helping Canadian families and our economy.

Indexing the CCB sooner will provide an additional $5.6 billion in support to Canadian families over the 2018–19 to 2022–23 period.

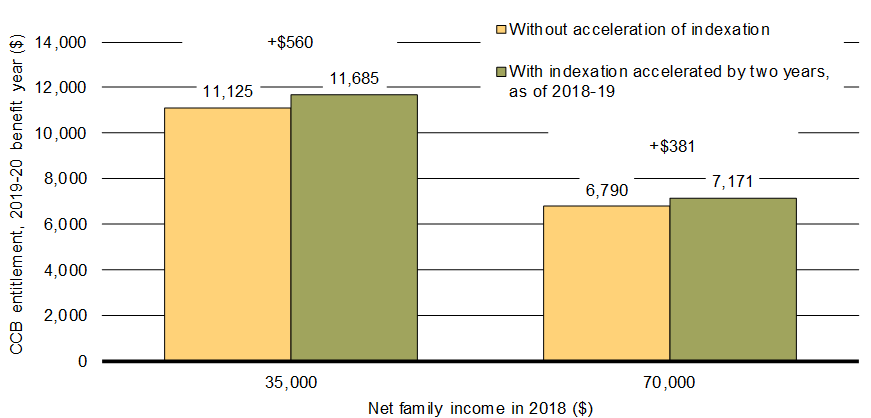

Impact of Indexing the Canada Child Benefit Sooner

For the 2019–20 benefit year, for a single parent with $35,000 of income and two children (one under the age of 6 and one aged 6 to 17), the accelerated indexation of the CCB will contribute $560 towards the increasing costs of raising their children.

Source: Department of Finance Canada.

Increasing the Working Income Tax Benefit for those Working to Join the Middle Class

Those working hard to join the middle class, including many low-income working Canadians, face financial barriers to joining or re-joining the workforce, including taxes, expenses, and the loss of supports such as social assistance. First proposed in 2005, the Working Income Tax Benefit (WITB) is a refundable tax credit that provides important income support and helps offset these barriers by supplementing the earnings of low-income workers (by up to $1,043 for single individuals without children and $1,894 for families under the federal design in 2017).

The WITB lets low-income workers keep more of their paycheque, encouraging people into the workforce, which has a long-term impact on income security and quality of life. In 2016, the WITB provided more than $1.1 billion in benefits to over 1.4 million Canadians.

To provide even more support and opportunity for those working to join the middle class, the Government proposes to further enhance the WITB by an additional $500 million annually, starting in 2019. This new enhancement will provide even greater support to current recipients by raising maximum benefit levels and will expand the income range of the WITB so that more workers can qualify.

Together with the increase of about $250 million annually already set to come into effect in 2019 as part of the enhancement of the Canada Pension Plan, these two actions will boost the total amount the Government spends on the WITB by about 65 per cent in 2019.

The Government will provide further details on the design of this new incremental enhancement in Budget 2018.

In recognition of the important role played by provinces and territories in providing basic income support, the Government of Canada has allowed them to make province-specific changes to the design of the Benefit to better harmonize with their own programs. As such, the Government of Canada will be consulting with provinces and territories before the enhanced WITB takes effect in 2019.

Increased WITB as Part of the Canada Pension Plan Enhancement

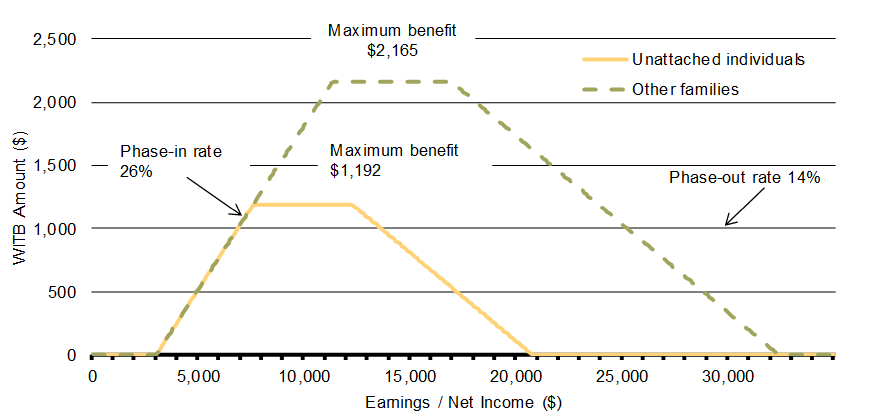

As part of the agreement to enhance the Canada Pension Plan, the Government increased benefits under the WITB, beginning in 2019, to roughly offset incremental employee contributions to the Plan. Under that enhancement, as of 2019, the WITB will provide a refundable tax credit of 26 per cent of each dollar of earned income in excess of $3,000, reaching a maximum benefit of $2,165 or $1,192 for families and individuals respectively. The benefit is reduced at a rate of 14 per cent of each additional dollar above the phase-out threshold (projected to be $16,925 and $12,256 for families and individuals respectively in 2019 after indexation with inflation).

Individuals who are eligible for the Disability Tax Credit may also receive a WITB disability supplement, with a projected value of up to $540 in 2019.

Chart 3.2 illustrates the maximum benefit, and phase-in and phase-out ranges for the WITB basic benefit for unattached individuals and other families in 2019 taking into account the enhancement associated with the CPP agreement.

Lowering Taxes for Small Business

Lower tax rates for small businesses allow them to keep more of their hard-earned money so that it can be reinvested to support growth and create jobs.

The Government's commitment—to both reduce the small business tax rate and address tax planning advantages for high-income earners—is a commitment to invest in our economy while ensuring fairness for all taxpayers.

By fixing a system that encourages wealthy individuals to use private corporations as a tool to gain an unfair tax advantage over the middle class, the Government will ensure that Canada's low corporate tax rates—including the lowest small business tax rate in the G7—are better focused on investments in the businesses themselves, in things like machinery, equipment, and job creation, rather than being used as a means to gain unfair tax advantages.

Having announced the next steps in its plan to provide fairness for the middle class by limiting tax advantages for the wealthy, the Government can now confidently propose to reduce the small business tax rate to 9 per cent from 11 per cent in 2015 over the next 14 months (10 per cent, effective January 1, 2018, and 9 per cent, effective January 1, 2019).1 The small business tax rate applies to the first $500,000 of active business income.

For the average small business this will leave an additional $1,600 per year for entrepreneurs and innovators to reinvest in their business, and create jobs.

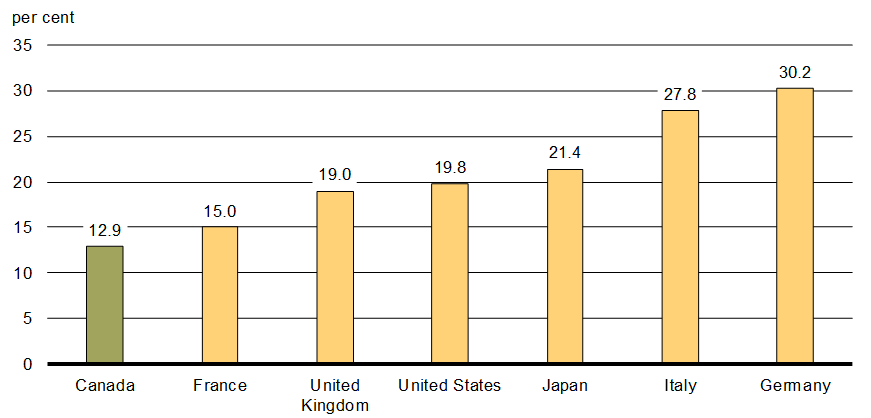

With these reductions, Canada's combined small business tax rate will decline from 14.4 per cent in 2017 to 12.9 per cent in 2019 (weighted-average federal-provincial-territorial) (Chart 3.3).

In addition to creating a beneficial tax environment for small businesses, the Government is advancing a number of initiatives that provide direct support for businesses. Budget 2017 announced that $400 million in new financing would be made available through the new Venture Capital Catalyst Initiative to increase the amount of venture capital available to firms and that nearly $1.4 billion in new financing would be made available through the Business Development Bank of Canada and Export Development Canada to help Canada's clean technology businesses grow and expand. In addition, Budget 2017 invested over $950 million in support of a small number of business-led innovation "superclusters", making it easier for innovators and potential customers to work closely together on research, development and demonstration activities to boost productivity, create jobs and drive economic growth.

A System That Works for the Middle Class

Our Commitment to Canadians

"As we reduce the small business tax rate to 9 percent … we will ensure that Canadian-Controlled Private Corporation (CCPC) status is not used to reduce personal income tax obligations for high-income earners rather than supporting small businesses."

The current tax system encourages wealthy individuals to incorporate in order to pay less tax. This means someone making $300,000, in some circumstances, can save about as much on tax as the average Canadian earns in a year—$48,000. That's not fair, and we are going to fix it. The Government is making changes to address tax advantages that disproportionately benefit the wealthiest Canadians, so that taxes can be cut for the benefit of the middle class.

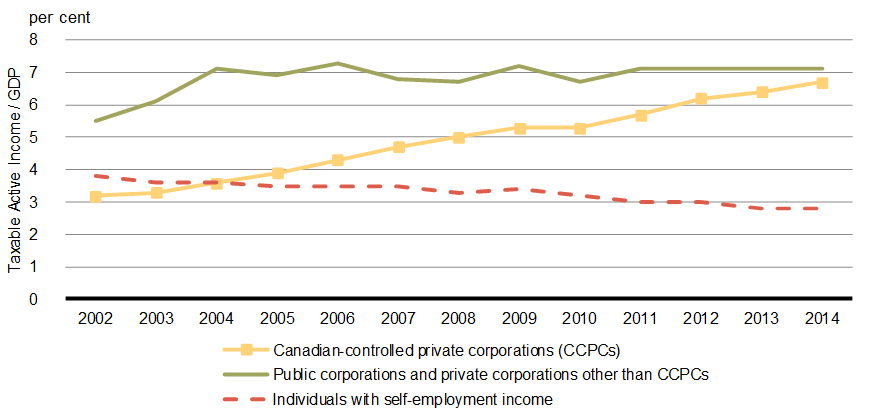

In its review of tax planning by private corporations, the Government identified significant recent growth in the number of CCPCs, and growth in their share of taxable active business income.

- Over the 2001 to 2015 period, the number of CCPCs has grown by 8.7 per cent per year, far surpassing a rate expected by economic growth. The number of active CCPCs has increased substantially, from 1.2 million in 2001 to 1.8 million in 2014.

- CCPC taxable active income as a share of gross domestic product (GDP) doubled from 2002 to 2014 (Chart 3.4). Meanwhile, the share of non-incorporated self-employment income declined and there has been little change in the share of income from public corporations and private corporations other than CCPCs.

The Government estimates that, in 2015, approximately $300 billion in passive investment assets were held by just 2 per cent of CCPCs.2 These assets, held by about 29,000 corporations, generated over $16 billion in passive investment income that year.

A Need for Action

Low tax rates designed to encourage investment have increased the rewards associated with tax planning in a private corporation, and have been partly used to opt out of higher personal income tax rates.

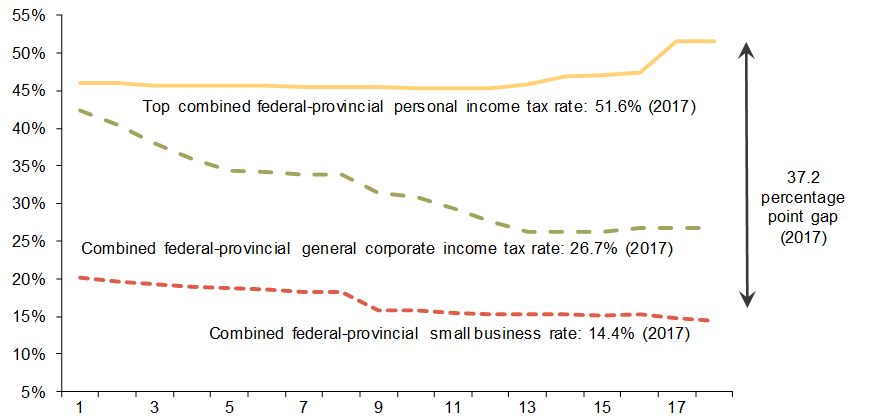

- The move towards more competitive corporate income tax rates since 2000 has widened the gap with top personal income tax rates from about 26 percentage points in 2000 to over 37 percentage points today (Chart 3.5).

The shift towards incorporation is gradually eroding Canada's tax base and is expected to continue, particularly as the services sector is expected to account for more of our economy in future years.

- The services sector now accounts for 71 per cent of GDP and 79 per cent of employment; in 2000 services accounted for 64 per cent of GDP.

- A shift to incorporation has been especially acute in services industries (e.g., financial services), and particularly so among professional services (e.g., lawyers, accountants and physicians)—the annual growth in the number of professional corporations has been 14.9 per cent from 2001 to 2015.

Chart 3.5

Federal-Provincial-Territorial Tax Rates

Action is needed to ensure that the tax rules apply in a fair manner and in a way that is consistent with their intent. If current trends continue, the significant growth in the use of CCPCs by high-income individuals will continue to weaken the tax base, increasing the tax burden on those who cannot benefit from incorporation.

As shown in Table 3.1, total taxable passive income is rapidly growing—at an average annual pace of almost 17 per cent over the 2010 to 2015 period. Annual growth in the number of new CCPCs over that period was 8.4 per cent.

| 2010–2015 Period | 2001–2015 Period | |||

|---|---|---|---|---|

| Growth in Number of Corporations | Growth in Total Taxable Passive Income | Growth in Number of Corporations | Growth in Total Taxable Passive Income | |

| Finance and insurance | 7.4% | 16.3% | 8.6% | 8.9% |

| Real estate, rental and leasing | 8.3% | 16.4% | 10.4% | 15.8% |

| Management of companies and enterprises | 7.0% | 15.8% | 8.5% | 8.6% |

| Professionals1 | 13.6% | 28.9% | 14.9% | 19.5% |

| Wholesale and retail trade | 6.1% | 21.7% | 5.1% | 7.0% |

| Agriculture, forestry, fishing and hunting | 7.5% | 15.6% | 6.9% | 12.5% |

| Construction | 6.9% | 16.4% | 7.6% | 13.0% |

| Other | 8.4% | 16.1% | 7.7% | 9.8% |

| All Sectors | 8.4% | 16.8% | 8.7% | 10.5% |

In the 2017 Fall Economic Statement, the Government proposes to strengthen small business competitiveness in Canada by:

- Fulfilling its commitment to reduce the federal small business tax rate to 9 per cent. The rate will be reduced to 10 per cent effective January 1, 2018, and to 9 per cent effective January 1, 2019.

In addition, in keeping with its commitment to address unfair tax advantages for the wealthiest, the Government proposes to:

- Move forward on restricting income sprinkling by private corporations, effective for the 2018 and subsequent taxation years, and to simplify the proposed measures and to provide greater certainty with respect to their application. Revised draft legislative proposals will be released later this fall.

- Move forward to limit the benefit of investing passively in private corporations. The details of the proposed rules will be released in Budget 2018, and will include an annual threshold of $50,000 of passive income for future, go-forward investments (equivalent to $1 million in savings based on a nominal 5-per-cent rate of return). There will be no tax increase on passive income below this threshold.

In light of feedback received from Canadians during recent consultations:

- The Government will not move forward with the proposed measures that would limit access to the Lifetime Capital Gains Exemption (LCGE).

- The Government will not move forward with the proposed measures relating to the conversion of income into capital gains.

The Government commits to apply future revenues from these proposed measures to further measures to support the middle class.

As announced on May 5, 2017, the Government also intends to bring forward legislative proposals to ensure that farmers and fishers are not inappropriately denied the small business deduction on income from sales to a cooperative.

In Budget 2017, the Government announced that its review of federal tax expenditures highlighted a number of tax planning strategies using private corporations, which can result in high-income individuals gaining unfair tax advantages over the middle class. In July 2017, the Government launched consultations to hear from Canadians, including small business owners, farmers, fishers and experts, on proposals to limit these tax planning strategies. In the course of this consultation, many Canadians indicated their support for these proposals but also raised significant concerns and areas where improvements were required.

The Government has listened and is committed to addressing unintended consequences. The Government's focus is on strengthening Canada's hard-working, middle class small businesses, their growth and their job creation, while targeting unfair advantages that largely benefit the wealthiest of Canadians.

As it further develops these measures, the Government will follow five guiding principles:

- Support small businesses and their contributions to our communities and our economy.

- Keep taxes low for small businesses, and support owners to actively invest in their growth, create jobs, strengthen entrepreneurship and grow our economy.

- Avoid creating unnecessary red tape for hard-working small business owners.

- Recognize the importance of maintaining family farms, and work with Canadians to ensure that the transfer of a family business to the next generation is not affected.

- Conduct a gender-based analysis on finalized proposals, to ensure any changes to the tax system promote gender equity.

Income Sprinkling

Through income sprinkling, high-income individuals can (depending on family circumstances) save thousands of dollars in tax in a given year. In some cases, someone earning hundreds of thousands of dollars a year can pay a lower tax rate than a middle class Canadian earning far less. In others, a single mother with two children under 18 can pay a higher tax rate than a married professional with two adult children.

To address these inconsistencies, and unfairness in the tax system, the Government intends to move forward with measures to limit income sprinkling using private corporations, while ensuring that the rules will not impact businesses to the extent there are clear and meaningful contributions by spouses, children and other family members.

Throughout the consultation period, the Government received feedback on the complexity of the proposed measures and potential unintended consequences. The Government also received feedback that the measures could create uncertainty in relation to how amounts received from a family business would be taxed.

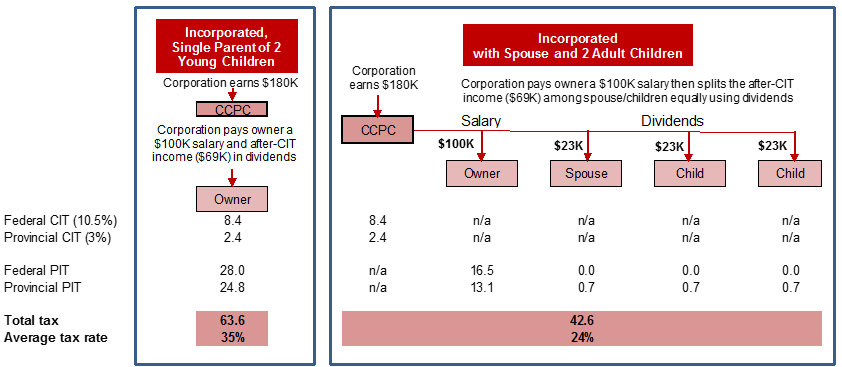

Sprinkling Income Using a Private Corporation—Owners of Corporations With Exactly the Same Income but One Owner Pays $21,000 More in Tax

Alicia and Brent are neighbours and business owners living in Nova Scotia.

- Alicia is a single mother with two children under the age of 18.

- Brent has a spouse and two children, ages 19 and 21; none of these family members has income.

Alicia's household pays about $21,000 more tax than Brent's household under current rules.

Both Alicia and Brent have incorporated businesses that earn $180,000 before salary and taxes in 2017. Each receives $100,000 in salary, and the remaining after-tax profits are paid out as dividends.

The difference is that Alicia's corporation pays all of the dividends to her. Total taxes (corporate income taxes plus personal income taxes) add up to $63,600 for Alicia's household.

Brent's spouse and adult children have no involvement in the business. They own shares in the corporation, for which they paid very little. Brent's corporation pays the remaining after-tax profits in equal amounts to these three family members as dividends. Total taxes paid by Brent's household equal $42,600.

Overall, Alicia's household pays $21,000 more in taxes (roughly 50 per cent) than the amount paid by Brent's household.

Under the proposed rules, given that Brent's family members do not contribute to his business, any dividends they receive would be taxed at higher marginal rates such that there would be no tax benefit to paying dividends to Brent's family members. Brent could therefore decide to have all salary and dividends paid to him. As a result, his household would pay roughly the same amount of tax as Alicia's household.

Income Sprinkling—Who's Affected?

- The vast majority of private corporations are not implicated. Only about 50,000 family-owned private businesses benefit annually from income sprinkling. This represents only a small fraction—roughly 3 per cent—of CCPCs.

- About 80 per cent of these families earn more than $125,000 in total income; 50 per cent of these families earned more than $200,000 in total income.

- Of the individuals that are sprinkling income, over 70 per cent are male.

- Family businesses will be unaffected if the spouse or adult children are meaningfully contributing to the business.

To address these concerns, the Government will simplify the proposed measures with the aim of providing greater certainty for family members who contribute to a family business. Specifically, the Government will introduce reasonableness tests for adult family members aged 18-24, as well as those 25 and older. These adults will be asked to demonstrate their contribution to the business based on four basic principles—whether they have made a contribution through any combination of the following:

- Labour contributions;

- Capital or equity contributions to the business;

- Financial risks of the business taken on, such as co-signing a loan or other debt; and/or

- Past contributions in respect of previous labour, capital or risks.

Taking into account the submissions made to the consultation, this fall the Government will release revised draft legislative proposals outlining the proposed changes addressing income sprinkling, which will be proposed to be effective for the 2018 and subsequent taxation years.

A number of stakeholders also identified potential unintended consequences associated with the proposed measures to address the multiplication of the LCGE. For example, concerns were raised about the potential impact on intergenerational transfers of family businesses. The Government will not be moving forward with measures that would limit access to the LCGE.

Sprinkling Income Using a Private Corporation—Genuine Family Business Arrangements Not Affected

Jacob owns a family farm in southwestern Ontario which he works with his wife Frieda and their adult son Herman. The farm is incorporated and earns $120,000 in net business income before salary.

- The farm pays Jacob $65,000 in salary and dividends.

- The farm pays Frieda, who does the farm's accounting and helps out on the farm, $30,000 in salary and dividends.

- Herman, who is 25 years old and works on the farm during the summer, on weekends and during breaks from university, receives $17,500 in salary and dividends.

This family will not be affected by the proposed rules on dividend income sprinkling because dividend allocations to Frieda and Herman are reasonable compensation for their contributions to the farm.

Once the small business tax reductions are fully implemented, the business will save an additional $750 which could be used to help pay for new farm equipment.

Passive Investments

During the consultation period, the Government heard from business owners that the flexibility afforded from savings accumulated in the corporation is important to their success. For example, savings can be held within a corporation to finance an upcoming business expansion or to save for a downturn. These savings are also sometimes used to provide flexibility to deal with personal circumstances such as for maternity leave, sick days or retirement—in such cases, savings held within the corporation can have both a business and personal component.

At the same time, Canadians pointed out that while there is a need for some flexibility, this needs to be provided in a manner that does not encourage wealthy individuals to have unlimited tax assisted savings over and above the RRSP and TFSA limits available to everyone else.

The Government will move forward with measures to limit tax deferral opportunities related to passive investments, while:

- Ensuring that investments already made by private corporations' owners, including the future income earned from such investments, are protected. The measures will apply only on a go-forward basis;

- Protecting the ability of businesses to save the funds they need for contingencies or future investments, such as the purchase of equipment, hiring and training of staff or business expansion;

- Including an annual passive income threshold of $50,000 (equivalent to $1 million in savings based on a nominal 5-per-cent rate of return) to provide more flexibility for business owners to hold savings for multiple purposes, including savings that can later be used for personal benefits such as sick leave, maternity leave, or retirement. There will be no tax increase on passive income below this threshold. Further details will be released in Budget 2018, including a technical description of how the passive income threshold will be applied; and

- Ensuring that as the Government moves forward with tax changes, incentives are maintained so that Canada's venture capital and angel investors can continue to invest in the next generation of Canadian innovation. The Government will work with the venture capital and angel investment sectors to identify how this can be best achieved.

The Government will also examine all deferral benefits from passive investments and will continue to assess key design aspects. For example, consideration will be given as to the appropriate scope of the new tax regime with respect to capital gains, including whether in certain circumstances the new rules should exclude capital gains realized on the sale of shares of a corporation engaged in an active business.

In this proposal, the Government remains committed to tax fairness, and the approach will ensure the measures are focused on a small number of high-income individuals who get the biggest advantage from existing rules. The Government will propose measures to limit tax deferral opportunities related to passive investments and release draft legislation as part of Budget 2018.

Of the 1.8 million active CCPCs in Canada in 2015, only about 325,000 reported passive income. Of this amount, it is estimated that 280,000 may have benefitted from deferral advantages. More frequently, CCPCs generate income from property that is considered incidental to their active business.3 In many cases, such income is not considered "passive" under current tax rules, and is not subject to the taxation regime that applies to passive income. This will not change. The object of the consultation is passive income that is over and above what is incidental to the business.

Similarly, the proposed changes to passive investment will not apply to income from AgriInvest, which is a self-managed producer-government savings account that allows producers to set money aside that can be used to recover from small income shortfalls, or to make investments to reduce on-farm risks—under the current system, investment income in an AgriInvest account is treated as active business income. The Government's intention is to maintain this approach.

Tax data show that:

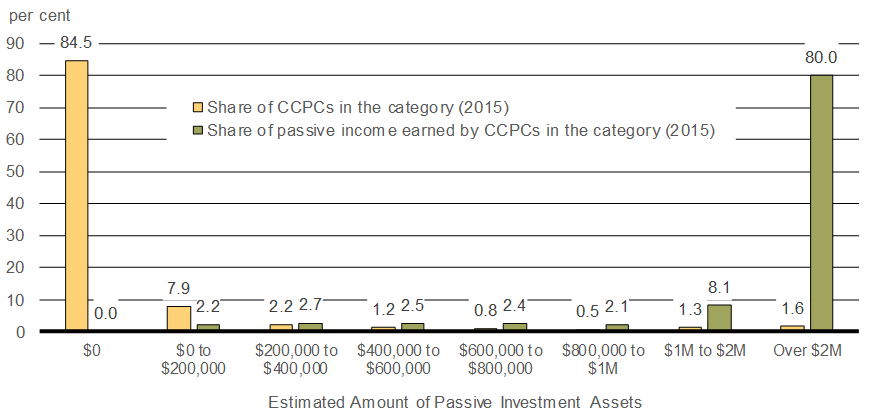

- Of the taxable passive income earned by the 280,000 corporations that may have benefitted from deferral advantages, 80 per cent is held by less than 2 per cent of CCPCs (Chart 3.6)—that group earned $16 billion in passive income in 2015, and held approximately $300 billion in passive assets.4

- About 97 per cent of CCPCs reported taxable passive income below the proposed $50,000 threshold in 2015. The remaining 3 per cent, those that reported more than $50,000, accounted for about 88 per cent of passive income reported in 2015.

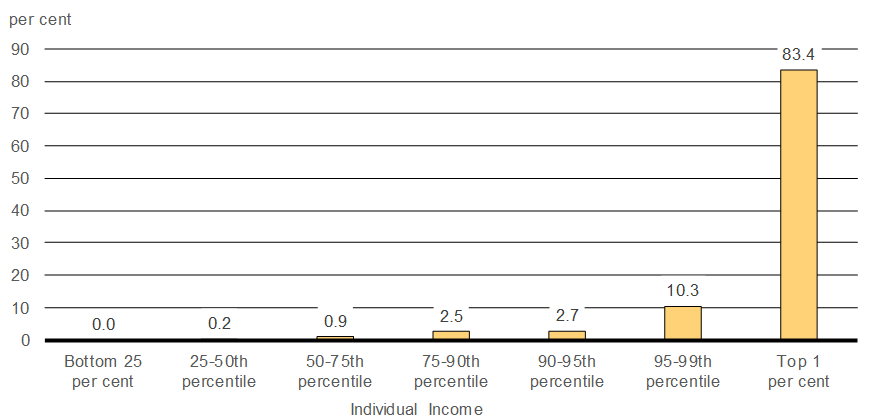

- Of the taxable passive income that can be effectively linked to individuals using tax data, 83 per cent is earned by those with incomes greater than $250,000 per year (Chart 3.7).

Notes: No data is available on the value of passive investments held in private corporations. The asset values used to produce the chart were imputed from passive income amounts reported by private corporations for tax purposes, using a hypothetical rate of return of 5 per cent. The amounts include capital gains, portfolio dividends and other investment income, such as interest. Data only include taxable passive income of CCPCs that may have benefitted from a deferral advantage.

Source: Canada Revenue Agency, T2 (Corporations) universe data set.

Source: Canada Revenue Agency, T1 (Individuals) and T2 (Corporations) universe data sets.

Benefits of Investing Passive Income

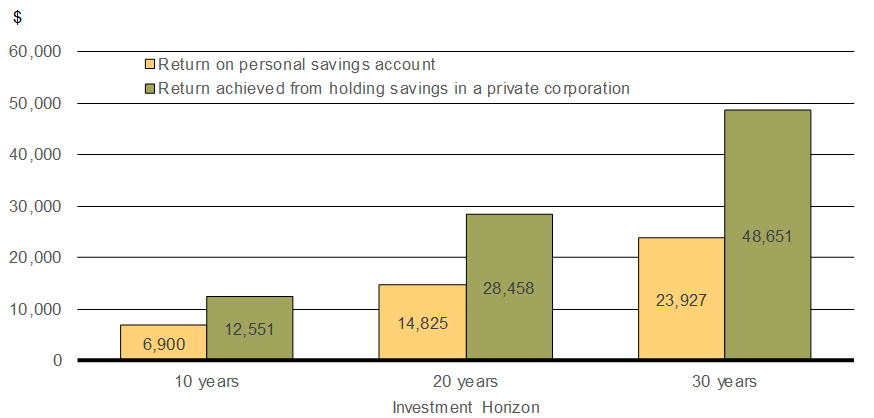

A high-income individual can realize significant tax advantages from holding passive investments in his or her corporation. The chart below shows the cumulative after-tax returns a corporate owner would achieve from investing the after-tax proceeds on $100,000 of income, in an asset generating 3 per cent interest annually, held within their corporation for 10, 20 and 30 years, compared to the return from saving in a taxable personal savings account. By benefitting from a lower rate of tax on business income, the amount of after-tax income that can be invested passively is larger than what they would be able to invest if they had distributed the income to themselves as salary or dividends. A corporate owner is able to earn after-tax interest income that is about 1.8 times more than they could realize at the personal level after 10 years (after distribution). After 30 years, the additional after-tax interest income from saving in a corporation is more than double what they could have obtained by saving at the personal level.

Chart 3.8

After-Tax Investment Returns for an Individual Investing Directly or Through a Corporation

Preserving Financial Flexibility

Expanding the Business

Victoria owns and operates a car dealership, and has aspirations of significantly expanding the repair and maintenance shop. She sets aside a portion of her profits every year and accumulates those savings inside her corporation.

- After paying herself a salary of $90,000, Victoria's corporation has taxable income of $180,000.

- Her corporation pays $24,300 in corporate income tax, leaving $155,700 for savings each year.

- Those savings accumulate inside the corporation and are invested in passive investment assets earning a 5 per cent rate of return.

- The passive income is subject to tax at the corporate level. That passive income grows over time, to reach $41,000 in the fifth year.

After five years, Victoria has accumulated some $840,000 in savings that she uses to buy equipment for her expansion.

- Her savings consist of $778,500 in after-tax profits plus $61,500 in cumulative after-tax interest income earned on her passive investments.

- The Government's proposals will not affect the amount of savings she has to buy equipment. No tax is payable when she reinvests the proceeds in her corporation.

Once fully implemented, the reduction in the small business tax rate to 9 per cent will enhance her ability to save for future business expansion. It will allow her corporation to save an additional $2,700 every year. Over five years, accounting for compounded returns, this translates into about $14,500.

Saving for a Downturn

Mohamed is a property surveyor who owns and runs his own surveying corporation. While he has been successful so far, he worries about the unexpected, and wishes to plan ahead for various eventualities.

- After paying himself a salary of $110,000, Mohamed has $23,000 of pre-tax corporate income, leaving him with about $20,000 to save per year in his corporation after he pays corporate taxes. By saving inside his corporation, Mohamed has the flexibility to use the money in his business, as needed. He also benefits from the lower small business tax rate, which leaves him with more money to use in his business. Once fully implemented, the announced small business tax rate reduction will allow him to save $345 more annually.

After five years, Mohamed managed to save $100,000 in his corporation, on which passive income is generated. These savings offer him the security of knowing he could manage short-term challenges to pay himself as well as pay for the salaries of his employees and other expenses for several months in case of a downturn.

Conversion of Income into Capital Gains

Canada's federal Income Tax Act has rules intended to address the use of various transactions by some taxpayers to avoid paying their fair share of taxes. Section 84.1 is one such rule and it is intended to address the conversion of amounts that would otherwise be taxed as dividends into lower-taxed capital gains. In the consultation paper of July 18, 2017, the Government sought to strengthen the income tax rules to curb tax planning strategies that seek to circumvent the intent of the Income Tax Act with respect to "surplus stripping".

The consultation raised issues with respect to unintended consequences and potential challenges with respect to intergenerational transfers of businesses, including farms. In particular, the Government in the consultation had asked Canadians for their views on how to better accommodate intergenerational transfers of businesses while protecting the fairness of the tax system.

Given these issues, the Government will not move forward with the proposed changes regarding the conversion of income into capital gains and the draft legislative proposals released with the consultation will not proceed, including the proposed effective date of July 18, 2017.

In the coming year, the Government will continue its outreach to farmers, fishers and other business owners to develop proposals to better accommodate intergenerational transfers of businesses while protecting the fairness of the tax system.

Gender-Based Analysis—Income sprinkling and passive income

The Government is considering whether actions to limit unfair advantages available to high-income and wealthy Canadians would impact men and women differently. This question is not straightforward. On the one hand, tax data show that a majority of owners of private corporations are men, and that men receive a greater percentage of dividend income from the corporations they control. That said, these unfair advantages are likely to affect individuals other than the corporation's controlling owner. For example, it is likely that existing tax benefits are shared with family members—the owner's spouse and children—or in the case of the sprinkling of income, that family members are part of the tax planning strategy.

As noted in the consultation paper, with respect to direct corporate ownership, tax data show that:

- Men reported 74 per cent of the net capital gains from the sale of qualified (private) small business corporation shares.

- Men received 66 per cent of small business dividends paid to individuals by CCPCs in 2014.

While the incidence of the measures is difficult to ascertain, additional statistics may assist in the determination of any gender impacts from the proposed measures:

- Data show that men represent over 70 per cent of higher-income earners initiating income sprinkling strategies. However, women are disproportionally represented among recipients of sprinkled dividends and income derived from trusts and partnerships (68 per cent and 58 per cent, respectively). While this income is of benefit for recipients, it also creates incentives that reduce female participation in the workforce. Increased participation of women in the workforce is a source of economic opportunity for individuals, but also a major driver of overall economic growth.

A detailed analysis of the gender impacts of the proposal that relates to passive income will be conducted before the Government decides on the final design of the new tax rules. That said, the measure will affect individuals that own and control private corporations and receive passive income, which are mostly men as noted in Table 3.2. The Government is committed to gender-based analysis, and will continue to refine its analysis of the gender impacts of the measures being contemplated with respect to passive income.

| Share of Total | ||||

|---|---|---|---|---|

| Income Range | Taxable Passive Income | Male Per cent of income range |

Female Per cent of income range |

|

| Less than $14,500 | (bottom 25 percentile) | 0.0% | 38.4% | 61.6% |

| $14,500 - $31,500 | (25-50th percentile) | 0.2% | 46.6% | 53.4% |

| $31,500 - $58,500 | (50-75th percentile) | 0.9% | 51.3% | 48.7% |

| $58,500 - $93,500 | (75-90th percentile) | 2.5% | 56.3% | 43.7% |

| $93,500 - $123,000 | (90-95th percentile) | 2.7% | 58.6% | 41.4% |

| $123,000 - $250,000 | (95-99th percentile) | 10.3% | 61.5% | 38.5% |

| More than $250,000 | (top 1 percentile) | 83.4% | 74.4% | 25.6% |

| All | 100.0% | 71.9% | 28.1% | |

1 The taxation of non-eligible dividends will be adjusted to reflect the lower small business tax rate in order to maintain integration of corporate and personal taxes.

2 No data is available on the value of passive assets held in private corporations. The $300 billion estimate is imputed from passive income reported by CCPCs for tax purposes, using a hypothetical rate of return of 5 per cent. The amounts include capital gains, portfolio dividends and other investment income, such as interest.

3 Income from property "that is incident to or pertains to" the active business, or income from property "that is used or held principally for the purpose of gaining or producing income from an active business" may be included in active business income for tax purposes. Whether income can be included in "active business income" is a question of fact.

4 No data is available on the value of passive assets held in private corporations. The $300 billion estimate is imputed from passive income reported by CCPCs for tax purposes, using a hypothetical rate of return of 5 per cent. The amounts include capital gains, portfolio dividends and other investment income, such as interest.

- Date modified: